David Woodruff gave a presentation devoted to Karl Polanyi and application of his theories to the current crisis in the Eurozone.

Continuing from his book Money Unmade, which touched upon the subject of barter in Russia during the 1990s, Woodruff has switched to Europe. He is currently investigating Eurozone macroeconomic policies and applying Polanyi’s ideas.

United by the end of the 1990s, European countries introduced common financial institutions such as a single currency and a single central bank. Until 2008, this project was seen as successful. However, with the collapse of the financial system in 2008, it was understood that the Eurozone is also vulnerable. Economic recovery began after the crisis was reversed in 2011, and is still ongoing. This is the “lost decade” as the cumulative growth from 2005 to 2015 is predicted to be only 1%. Another aspect of the recession is unemployment: although unemployment was observed in the U.S. and Japan it began to fall there, while in Europe it continues to grow.

There is a so-called Keynesian recipe for struggle with recession, or “liquidity trap.” A crisis occurs when a decrease in earnings causes a decrease in budgetary revenues, as well as unemployment and poverty, which also lead to additional budget expenditures. In this case, demand is replaced by the state: economic growth resumes and the crisis goes away.

Where does the state get the money for this stimulus? It borrows from the people who hadn’t previously invested in the economy. This is the liquidity trap—when people prefer to keep their money in a rapidly convertible form rather than investing in long-term projects. People see that government debt is rising and thus don’t want to invest in the government because the debt will have to be paid sooner or later.

Of course, a budget deficit and national debt are less fearsome during a time of economic growth because the latter eliminates negative effects. This argument is problematic, however, because it is based on the idea of fiscal austerity.

Fiscal austerity is a vicious circle. Economic downturn leads to a decrease in revenue and an increase in budgetary payments, which increases the budget deficit. This, in turn, leads to attempts to economize—spending cuts and tax increases, which again lead to economic downturn.

In this sense, the Eurozone policy is contradictory. The European Central Bank, taking measures against the crisis, has numerous credits in small stakes, while national governments save banks with monetary injections. These measures, however, are limited because they rely on the effects of fiscal austerity. There is a stalemate: the struggle with the crisis exacerbates it.

Here, it’s necessary to turn to Karl Polyani and his renowned book The Great Transformation, written in 1944. This is a classic work not only for economics, but also political economy and economic anthropology. The basic idea is that the self-regulating market is not the result of spontaneous social evolution, but the result of conscious construction—the market was specially invented. By itself it leads to catastrophic consequences, since if wages depended only on supply and demand, people would starve to death en masse when the price of labor became too low. This is what is called the “double movement.”

Thus, the state forcibly interferes with the price mechanism to protect society from the market—by paying for social benefits, for example. This is called the “protective counter-movement”. Polanyi believed that he revealed through this the institutional mechanism for the collapse of civilization. World War II, in particular, was a reaction to the Great Depression, which, in turn, arose due to the Gold Standard system.

With the Gold Standard, money holders could exchange money for gold at any time. The more gold available for exchange, the more money there could be in the economy, and thus correspondingly higher prices. The exchange rate of national currencies, backed up by gold, was fixed.

Thanks to the Gold Standard the economic system remained balanced. In the instance of a trade deficit, when importing and buying of goods was greater than selling, there was a release of gold, leading to a decrease in the quantity of money in circulation and an attendant decrease in prices in the country. From the decrease in prices came an increase in competitiveness (since prices are higher in other countries), which led to an increase in exports and stabilization of the trade balance.

As Polanyi argues, the problem is that this mechanism is not considered part of societal self-defense. Reduced prices in a country are trouble for businesses because their profits fall. Protective counter-movements begin for labor (unemployment benefits are paid), land (including support for agriculture), and the organization of production (monetary supply expands). Because of this the system doesn’t work, although it functioned normally in the 19th century.

The Great Depression arose because of a trade imbalance, which in turn occurred because of a poor relation between the exchange value of gold parity with real prices. Prices did not converge because of a protective counter-movement: trade deficits financed the expansion of international loans.

This became the bomb that exploded the economy. On the one hand, the turn in international credit and on the other, the currency panic that limited the autonomy of central banks led to fiscal austerity. For owners of large capital, the Gold Standard allowed control of the labor class, which the Labour Party stubbornly resisted. The financial market governs with the help of panic, which is used as a weapon of political influence. Thus, the market opposes democracy. The struggle between the two weakened democracy and led to the catastrophe that we saw in Germany.

There are three possible outcomes of such a stalemate. The first is to completely abandon the Gold Standard (as the U.S. did, leading to Roosevelt’s New Deal).

The second is the marginalization of democracy in favor of deflation, which led to the rise of Hitler. The third is the abandonment of the Gold Standard, but only after the political defeat of the Labor Party, as happened in Great Britain. There, the mentality of the Gold Standard was nonetheless preserved.

We will illustrate panic as a weapon of political influence with the case of Great Britain. In the summer of 1931, Laborites were in power. The economic situation was complicated: a budget deficit, poor foreign trade, and mass conversion of pounds into gold. The main political question: how to balance the budget?

There are two classic answers. Either tax the rich, or cut back on unemployment benefits. The Laborites could not make a decision, and were therefore removed from power.

This was due to the deputy head of the Central Bank of Britain, Mr. Harvey. He insisted on the reduction of social benefits (with which the Laborites categorically disagreed) after which he said the country’s gold reserves would last only three days. This caused a split in government, and the leftists resigned.

Karl Polanyi puts forth two important ideas. First, that a stalemate in the economy may be the result of contradictions between the protective counter-movement and the orthodox policies of the Gold Standard. Second, in order for financial policy to work as a political weapon it is necessary for someone to intimidate and persuade others that there is no other way of solving a problem.

Eighty years later the Eurozone crisis is very similar to the Great Depression—trade imbalances are growing. Prices are not converging but rather diverging and people are investing where prices are rising, because it is profitable.

The paradox lies in the fact that there is no longer a Gold Standard as such, and the European Central Bank can calmly deal with financial panics. So why is there a similar situation?

There is room for self-justified panic in the government bonds market. The increase in the budget deficit leads to an increase in the interest rate on bonds, which increases the cost of maintenance loans, which leads to a deficit. There is one way to deal with this in the conditions of a panic—the state purchase of bonds in unlimited quantities.

According to German Federal Bank President Jens Weidmann, the growth of interest rates should not be the basis for financial intervention by the central bank in a given Eurozone country. This reinforces financial panic, because it deprives government guarantees, and capitalists have mixed feelings about this. Here, we can see the incarnation of the doctrine known as “Ordoliberalism.”

Ordoliberalism is a German variation of Liberalism. In Germany there aren’t problems with a strong state, since it is namely the state that creates the market. But this presents another problem: how, then, is government limited? It must be a legal state in the Roman sense—without discretionary decision-making powers, but only according to the rules.

A dilemma arises: what to do if an action indicated by law leads to economic disaster? According to ordoliberalism, this almost never happens. The long-term effects of adherence to laws cover the short-term deficiencies.

We can give several examples of ordoliberalism in action. Weidmann argues that the government should not redeem bonds because there is the danger of muting market signals. In his words, “We should all become competitive together.” But this contradicts the very idea of competitiveness, when someone is always in a better position than the other. Here Weidmann speaks about something else—about virtue.

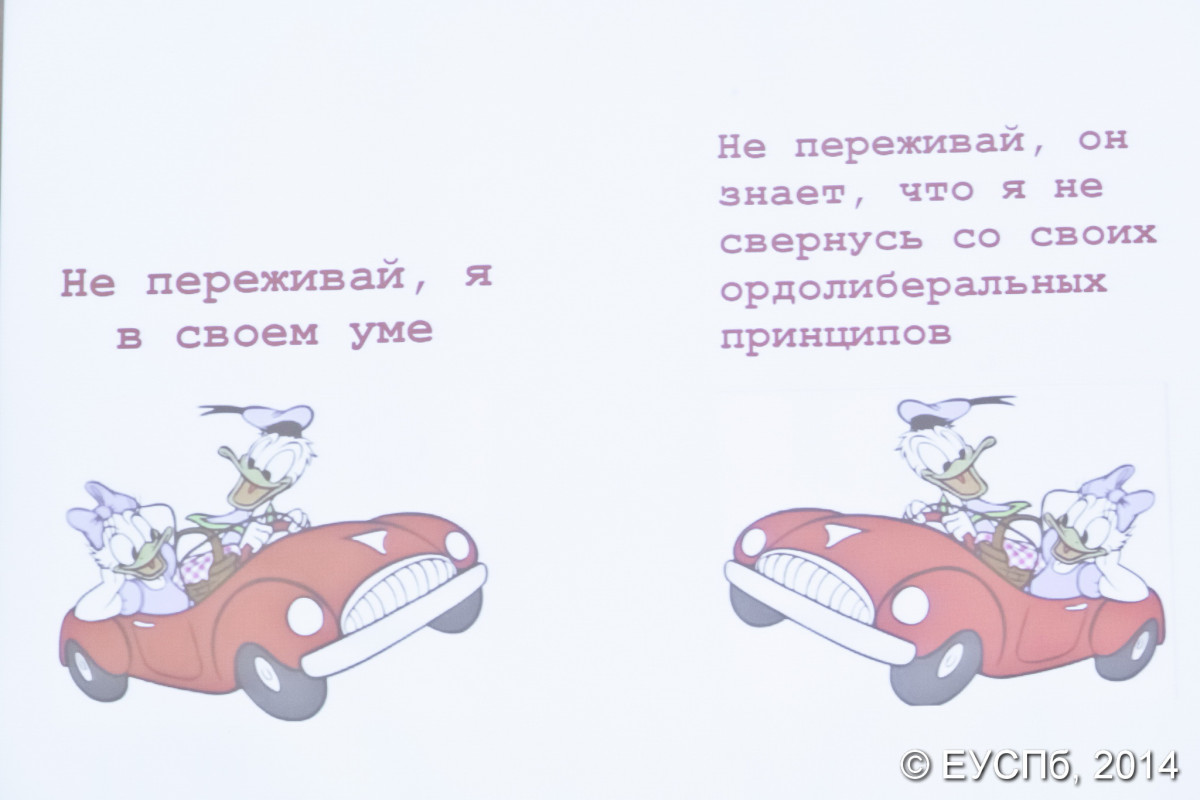

Why do ordoliberals have such influence, and are their policies working? We can examine this from the point of view of game theory, or, more precisely, the game of “chicken.” The everyday example is when two drivers go at each other at high speeds. One of them must turn at the last moment because otherwise they both will crash. The one who turns loses, becoming a “chicken.” Ordoliberals win politically because their opponents believe that ordoliberals will never swerve from their principles.

In conclusion, Woodruff noted that, in his opinion, there is not enough in Polanyi’s approach for analyzing contemporary European economic policy. First and foremost, there is the specific political structure of the Eurozone, which differs from the structure of the nation state.

Aleksey Knorre